The Revenue Equation, PMF at Wakefit, and Benchmark Capital

Sajith Pai's incredibly irregular newsletter #18

Welcome to the latest and long-delayed edition of my irregular newsletter! A hearty welcome to the 186 new subscribers who have signed up since my last newsletter, and will receive their first ever Sajith Pai newsletter. How exciting!

Quick housekeeping announcements. The newsletter has two permanent sections. Writings - where I usually write and / or refer to one or more original pieces, typically about venture or the startup ecosystem, and, Readings - about what I read and learnt about. My reading diet is tilted heavily in favour of podcast transcripts (and of course books) and against articles / newsletters. This will naturally reflect in the reading list.

Writings

The Revenue Equation, KPIs, and Controllable Input Metrics.

I wrote a post on how startup founders should think about business metrics, how to derive metrics relevant to their businesses, and rank order them, through building out a revenue equation. In the post, I highlight why Controllable Input Metric(s) (and not North Star Metrics) are the most important metrics for founders to focus on. In addition, I cover how to set incentives to drive desirable behaviours and nudges. Link to the piece.

PMF Convo #1: Interview with Chaitanya Ramalingegowda of Wakefit

I am presently writing a book on product-market fit or PMF, a seminal concept in the startup world. It is a topic I have been obsessed with for a while now, given that a large part of my success rests on helping my portfolio achieve PMF. In that regard, the lack of a practical guidebook / playbook for early-stage founders on this topic has always puzzled me. In fact, for such a key concept, there is no one agreed definition either. So, I set out ambitiously, to correct this, hoping to create a playbook or guide for early stage founders to systematically work towards PMF.

As part of the writing, I have been doing interviews with founders, to get their perspective on the topic, and related aspects such as Go To Market, Metrics, Pivots etc. These interviews have been consistently interesting and illuminating. So, I thought it would be useful for other founders and operators in the startup ecosystem to learn from, and decided to make it publicly available, after getting approval from the founders. Here is the first of the interviews, with Chaitanya Ramalingegowda of furniture + mattress eretailer Wakefit.

Link to the transcript (edited) of my conversation with Chaitanya of Wakefit.

What I found interesting from the conversation with Chaitanya

Chaitanya’s definition of PMF and how they worked towards that in Wakefit is influenced heavily by his and Ankit’s past failures. He sees PMF through the lens of sustainability and profitability. Growth doesn't get mentioned at all.

A key cultural trait at Wakefit is close customer listening. Chaitanya’s lunch time staple is listening to customer recordings. Team members are encouraged to talk to customers to gather feedback. Meesho and Classplus too have similar cultures of close customer listening.

One of the areas he works with his angel investee founders is on ensuring they are in the right headspace and are not stretching themselves thin on the financial or mental health front.

Related to #1 is a pattern that I saw consistently across all my interviews. Founders solve for growth usually (barring exceptions like Chaitanya who solve for profitability). They do not think formally about PMF or the mechanics of that as much as they think or obsess about growth. PMF or the lack of it seems to be an aftereffect of their actions around growth. If anything, PMF seems to be a VC perspective or outlook largely. At least this is what the interviews thus far have told me. Mind you, I have only done interviews of Indian founders. It will be interesting to contrast this with views of US and European founders.

Readings

I picked up David Rubenstein’s (cofounder of PE firm Carlye) book ‘How to Invest’ at the Mathrubhumi Bookstore at the Kochi Airport (easily the best airport bookstore in India with a kickass graphic novels collection). It is a collection of interviews with leading investors across different asset classes - Sam Zell (Real Estate), Paula Volent of Rockefeller (Endowments), Ray Dalio (Hedge Funds) and so on. Each chapter is one interview.

Overall, I didn't find the book very impressive. We are living in the golden age of the interview (given how 1:1 podcasts have become the dominant form of knowledge transmission) and given the podcast transcripts I read, I now have a high bar. David’s work didn’t clear the bar.

In the venture investing space, it had Mike Moritz of Sequoia and Marc Andreessen of A16Z. I got the two chapters scanned into pdfs for your reading pleasure. Enjoy.

Mike Moritz’s interview - Link to pdf

Marc Andreessen’s interview - Link to pdf

One interesting contrast between the two firms is how they make decisions. At Sequoia they require unanimity (Moritz: “It’s been frustrating at times over the years, but on the whole it’s served us well.”) whereas at A16Z they have a ‘single trigger-puller’ system, i.e., any of the present 22 General Partners can make a decision without a vote.

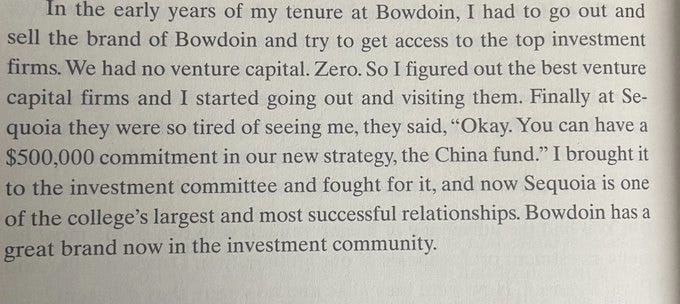

My favourite chapter was the Paula Volent interview. Originally an art conservator she transitioned into the world of investing, joining the Yale Endowment, following her MBA from Yale. At the Endowment, she started off initially by helping David Swensen with his book Pioneering Portfolio Management, and later moving into investing full time. She moved from Yale to become the CIO (Chief Investment Officer) at Bowdoin College, a tiny liberal arts college in NorthEastern USA. Under her watch, Bowdoin outperformed most other endowments including Yale’s. She recently moved to become the CIO for Rockefeller University’s endowment.

I found the below passage in the Paula Volent interview fascinating.

Just as the best founders get begged by VCs to take their money, the best VCs too get begged by LPs to take their money. This is why the venture business is often called access class (as opposed to asset class). It is so hard to get into Sequoia, or Benchmark or any of the elite top tier funds (and thanks to ‘persistence’ they continue to be top decile, fund after fund) that the right to continually invest in Sequoia's funds, held by its LPs (Limited Partners) is one of the great investment assets an endowment can hold.

I haven’t read (or rather completed) too many books since the last newsletter. A bunch of the books I am reading are interview books like How to Invest, Founders at Work etc., which have one interview per chapter. These are kinda hard to read in one or two sittings. Still, I should wrap these up soon.

One book I managed to read over the course of a day was eBoys by Randall Stross. This is a twenty-two year old book, published around the time of the dot com boom, and covers two years in the life of Benchmark Capital, including their eBay investment and the IPO. They invested $6.7m in eBay mid-‘97 picking up a 22% stake. In under two years, eBay was trading at $21b, 1000x up! eBoys is a fascinating look at how a VC firm sources and picks investments. In parallel, it also chronicle’s eBay’s extraordinary rise. On the whole, an excellent read.

The book had been lying on my shelf unread for a while. What spurred me to pick it up was the excellent podcast double bill on Benchmark Capital by Acquired. (Episode One, Episode Two - both have transcripts as well)

Benchmark is an extraordinary fund. It is tiny. The latest fund is just $425m. Even though it can raise a gazillion dollars given its success backing generational companies like eBay, Uber, Twitter, Instagram, Snap etc., it doesn't. It intentionally chooses to remain small and boutique-y. In fact they don't do growth or opportunity funds, even. Even more extraordinary, the Partners all have equal share in the carry as well as in the GP partnership. Always! There isn’t a fund like this.

The podcast has a lot of colour and context on its evolution, and how it is able to survive and thrive via several key cultural frameworks. The venture nerd in me totally geeked out on this one. Below is what I found most interesting from the podcast.

Equal rewards for the Benchmark partners mean that everyone is incentivised to contribute to a winner, irrespective of who takes the board seat or led the deal. Teamwork evolves out of incentives. Over time, cultural norms have evolved that whenever anyone hesitates that they are unable to put in 100%, they retire from the partnership.

A powerful forcing function for the camaraderie is the long monday meeting (which is famously without an agenda) and the dinner that follows that evening with an external guest. They also don’t have a CRM and do not write investment memos. From the podcast (Part II) “The artifacts, they live in the memories and the lived stories of the partners. If there's a curiosity in that direction, call up Matt, call up with each other. Call up Matt, call up Bill. Those learnings, those stories, that wisdom sort of still walks.”

LPs do quibble about the fund size - they do wish it could be larger. Their largest LP (very likely Horsley Bridge, which has invested in every single Benchmark fund) only deploys $25-30m in them. The retiring GPs all become LPs apparently which further squeezes the institutional LPs’ ticket size.

Here is a pic of the Benchmark office. All the partners sit around a round table, and not in cabins / personal offices. (from the show).

From Benchmark to Sequoia, another equally if not more successful venture firm.

Sequoia has succeeded with a very different approach. Sequoia raises far larger funds (it has raised $14 billion across all its geographies this year), has teams across the globe, operates across different stages - seed, venture, growth etc.

I read transcripts of three podcast episodes featuring three different Sequoia investors - its US / Europe Head Roelof Botha (Tim Ferriss podcast), and US-based Partners Jess Lee (who is also their Chief Product Officer) and Ravi Gupta (both on Colossus / Invest Like The Best). All three are consistently interesting and informative in their own way. Here is what I learnt about Sequoia and found the most interesting from the three episodes

1 - Sequoia has a strong writing culture. When we think of writing cultures we think of Amazon and Stripe, but it seems Sequoia too has an evolved writing culture and practice. Ravi Gupta: “It's a very written culture. People will say things like, "This was not a very good memo. I don't know how to help you make the decision here because I don't have a lot of my questions answered." That is a really painful thing to hear amongst the small group. Sequoia's pretty small on the investment team. The growth team partner discussion is 10 or 11 people. They're all people you know and respect, and you care about their opinion. When someone says it's not a very good memo, it's tough, but that will happen. It will happen where someone will say, "I really think this is a really important company and we really need to invest." And someone will say, "I just don't understand what you're saying because of X, Y, and Z."

One particularly interesting element of the memos are Pre-Parades and Pre-Mortems which were introduced by Roelof Botha, following a conversation with his fellow Square (now Block) board member Larry Summers. Pre-Parades ask you to imagine a world where the product / startup is an outrageous success, and then you work backwards to detail out what led to the success. Pre-Mortems work the other way around asking you to imagine failures and work out what was the root cause, so you can take corrective action. Botha says that every two years they do a Pre-Parade and Pre-Mortem for Sequoia too.

2 - Sequoia invests heavily in tech to aid in both ‘minding’ and ‘finding’. They have a founder mobile app and portal called Ampersand, where a founder can look up answers to questions around product, marketing, org-building etc., as well as DM other founders. They also have a data science platform (there is a large tech and product team based in Bangalore from what I have heard which develops these) that provides signals and data to the Sequoia team - helping identify interesting pipeline opportunities as well as validate that the company is on the right track. Jess Lee says: “On the sourcing front, one of our partners, Bogomil, led an investment in a company called Infracost. Infracost has an open source component. And so we were able to see in GitHub that company was inflecting. And so, Bogomil was able to reach out maybe one month sooner, maybe before they were raising, and was able to establish that relationship. And we look at all different kinds of signals. “ Incidentally the Botha episode mentions an older Sequoia product called Early Bird, a system designed by a partner, Jim Goetz, which helped them identify Whatsapp early.

3 - It is interesting how large the platform teams at Sequoia are. Everybody talks about A16Z, but Sequoia’s teams aren’t small either. Botha: “Today, our team at Sequoia US and Europe is about 180. Like I mentioned earlier, the investing team is still pretty small. We have 25ish investors in our business, but we have marketing capabilities, we have data science, we have engineering, we have product. We obviously offer talent services to our portfolio companies. We have a big finance organisation now that manages the complexity of all of this. And so, we’ve just changed as a business to be able to serve founders.

The business has gotten more competitive, and so you can’t just be money. As you pointed out earlier, there’s just so many people who are willing to write checks. That is not a differentiator. What is it that I’m offering an entrepreneur that makes him or her choose to work with me? Because they think that I have a disproportionate impact on their chance of success, right? That’s partly me, my experience. My partners, what we bring as a team, and what are the other services around our partnership that we can deliver to help you succeed? “

A couple of other podcasts I found interesting and insightful.

First up, Alice Bentinck of Entrepreneur First (EF) about the EF model on Colossus / Invest Like The Best.

EF is a fascinating distinctive accelerator model. Unlike YC, here you join as individuals and then form teams of two and then conceive an idea, develop a product and launch. Like YC, there is a certain funding that comes with the program, and also a demo day.

I found the episode fascinating, especially because I have a strong preference for founders who have known each other for a long time. In fact, I seek this in the founding teams I meet. I believe that this makes the founding journey easier, as uncomfortable discussions are easier between two or three people who have known each other a while. I once passed on one EF startup for this reason. In that regard, this episode was an eye-opener for it gave me visibility into an alternative approach, and one which seems to be working as well.

One of my key learnings about the venture business over the past few years is that there are diverse approaches to success in venture. If strategy X works for you, then there will be someone else using strategy Y, which is the opposite of X. Don't knock Y just because it is different from X, e.g., we saw how the decision-making styles of A16Z and Sequoia differ. So similarly there could be a Sajith Pai finding a Classplus attractive because the founders have bonded since high school test prep coaching, while an EF is able to bring two strangers together, and fund them.

The following were my takeaways from the episode / what I found interesting.

1 - Bentinck’s view on how EF’s competition is not other accelerators but whatever socially desired career option is the default for highly ambitious young women and men (NYC, London have Finance, whereas in Singapore and Paris it might be Government etc.) It is these social accepted default ‘ambition tracks’ that limit the supply of founders outside Silicon Valley, and it is EF’s desire to break these norms.

2 - How they have structured social norms inside the EF Program to celebrate breakups of teams - celebrating pairs breaking up so that each of the founders can connect and explore other cofounders. “The primary thing that we focus on is how to have difficult conversations with your co-founder. And the reason we do this is because we want individuals to get into and out of teams as quickly as possible. So we want to get you into a team before you feel ready, and then we want to get you out of the team the moment that you begin to have doubts. Because the opportunity cost of being in the wrong team with the wrong co-founder is so insanely high. Team building at EF is only eight weeks long, which feels like a reasonably long period of time, but actually when you're in, it's incredibly short. “

3 - Alice: “One of our strong beliefs is that your best friend is not your best co-founder. And if a co-founder is going to be one of the most expensive decisions you ever make in your life, assuming you're successful, you give away half your company to this co-founder, there's literally nothing more expensive that you could do, you really need to treat it like a hiring process rather than like a friendship development process.”

The other podcast I enjoyed was the Zetwerk founder, Amrit Acharya’s appearance on Sequoia India / SEA’s Moonshots podcast. I found Zetwerk’s journey to PMF, through two pivots fascinating. They started off initially selling SaaS software to make procurement of industrial parts easier, then a marketplace and finally a full stack managed marketplace for manufacturing. The journey was successful because they listened closely to what the customers were saying, or more importantly did not say, but mean.

Amrit: But at the same time, all these customers were asking us, “Can I use your software to discover new suppliers?” And, nobody was saying this in a very active way, but if you listened enough, that was what they were asking. That’s when we pivoted the business.

Shailesh Lakhani, the Sequoia partner who cohosts the episode says “Customers don’t know exactly what they want, but they can give you clues and hints that can lead you to figure out what is the real opportunity that is in front of them.“

Another perceptive observation from Shailesh: “ I think another key insight that Zetwerk had in the early days was that they are the best users of their software themselves. That a customer wouldn’t be able to get the most out of it because the organisational mindset, the systems and the processes, and the motivation to use it well, is something that they have much more in- house than they can imbibe on a customer. “

A few articles I enjoyed reading -

Analytics and Product-Market Fit - Really good post by the Analytics team at Meta on how to validate PMF through measuring and tracking the “three vital signs of PMF - stable retention, sustainable growth and deep engagement”.

Grit or Quit? Tactical Advice for Founders Facing Tough Decisions - Annie Duke (yes, the Poker champ and writer who is now the Special Partner for Decision Science at First Round Capital) writes about when to quit and walk away. This is based on her book ‘Quit’ on the same topic. Good read with two very useful frameworks on how to approach quitting - solve for the hardest part of any project so that you know whether it is worth proceeding on and or solvable, and secondly set specific kill criteria in advance. “A simple way to develop kill criteria is with ‘states and dates. If by (date), I have/haven’t (reached a particular state), I’ll quit.”

This 6-part series on how to launch and grow a B2C / Consumer startup by Lenny Rachitsky was very very good. Lots of gold here - especially Part 5 which covered Retention, and Product-Market Fit (paywalled).

Bye

That is all for now, folks. Feedback in the comments or at sp@sajithpai.com (if you want to send me a pitch, then email at sp@blume.vc please).