Darwin, Type II errors, AI-generated birthday menus, & Shrinks for VCs

Sajith Pai's somewhat irregular newsletter #22

Welcome to the 22nd edition of my rather irregular newsletter! For the 122 new subscribers who have signed up since my last newsletter in May, enjoy your first. Fortunately you haven’t had to wait as long as your predecessors!

Quick housekeeping announcements. The newsletter has two permanent sections: Writings - where I usually write and / or refer to one or more original pieces that I published in the previous months, typically about venture or the startup ecosystem, and Readings - about what I read and learnt about. My reading diet is tilted heavily in favour of podcast transcripts (and of course books) and against articles / newsletters. This will naturally reflect in the reading list.

This is a long newsletter - think of it as akin to a monthly magazine from me (only the frequency may not be monthly!). I don’t know if you can read this entire newsletter (and peruse the links) in one sitting, and even if you do a second run (or more which I very much doubt), you will have to pick and choose what to focus on. A good way to read this newsletter is to certainly read my original writing below, and then glance through the rest and pick 1-2-3 items that pique your interest. Anything more is a bonus.

“A painting in the style of Herge, of a man typing out a newsletter on a Bloomberg Terminal in New Delhi in an Indian setting”; DALL-E

Writings

I read Nalanda Capital founder, Pulak Prasad’s recent book ‘What I Learned About Investing From Darwin’ over the past few weeks. Nalanda has an exceptional track record, and Pulak is known as much being super-reclusive as for his track record. So the book since it was announced, was keenly awaited by the public investment community.

The book describes Nalanda Capital’s investing philosophy and how it compares with principles and practices he sees in the field of evolutionary biology, of which he has been a student of. I found it an interesting and enjoyable read. After reading the book, I tried to contrast and compare the principles Pulak espouses in the book to my field of venture investing. Here is the result.

A VC’s Perspectives on a Legendary Public Market Investor’s Book

Pulak is a student of evolutionary biology and in his first book, he uses readings and findings from his readings of ecologists and evolutionary biologists to illustrate key investment principles. It is an interesting read, though some evolutionary principles seem to translate better to the world of investing, while some seem forced. Nonetheless, it is a fun, easy read. Those who like to read books on public market investing will find it the most useful. As a private market investor, and one who operates in a field and style far removed from Pulak’s, I still found it useful and interesting.

In this essay, I will first layout out the broad thrust of Pulak’s book, distilling his key ideas. In the next section, I will look at how they contrast and compare with venture investing, the field where I work.

Distilling the book

A bit about Nalanda before we start. Nalanda is known for its disciplined investing style, selecting high quality businesses after considerable research, and buying into them when they become available at discounts during market crises. They typically buy deep when they enter a company and are almost always the largest institutional shareholder. ₹1 invested in Nalanda’s first fund in June ’07 would have been worth ₹13.8 in September ’22. The same amount invested in the Sensex would have been worth ₹3.9. At 20.3% annual rupee returns net of fees, these are incredible results. Now to the book.

Pulak starts the book by laying out Nalanda’s investing principles. These are

Avoid big risks.

Buy high quality businesses at a fair price.

Be very lazy (in buying and selling).

The book is also structured around these principles, with a section and chapter set, for each of the principles.

The bedrock of their philosophy is that there are very few good investments in the market. Given this, it is better to reduce errors of commission or Type I errors (investing in bad companies) than errors of omission or Type II errors (missing out on good companies) – because the errors of commission cover a much larger number of outcomes. In pages 20-22, he illustrates this with examples and shows how reducing Type I errors or errors of commission dramatically improve investment outcomes, but reducing Type II errors or errors of omission doesn’t help as much, because there are far more bad companies vs good ones (typically, there are about 25% ‘good’ companies in any listed universe he says). The best investor has to be the best rejector, he says.

How do they reject? They first avoid risky businesses. These are businesses with poor corporate governance, businesses in turnaround situations (as typically these don’t work out), highly leveraged businesses, those who keep growing through inorganic means, and finally those with unaligned owners (govt-owned businesses, subsidiaries of foreign businesses etc).

Their investable universe is ~800 Indian businesses (with market cap of >$150m). They reject ~350 businesses for reasons shared in the earlier chapter (governance, leverage, turnaround, excessive M&A, non-aligned owners etc). Of the remaining 450, they use historical ROCE (Return on Capital Employed) to bring it down to ~150.

In nature, selecting for just one trait can influence many other behavioural and physical qualities of an organism, like the example he gives of selecting for tameness in Siberian Foxes which turned them into doglike beings with curly tales, spotted coats etc. Per him, ROCE is the equivalent of tameness on the business end, in turn correlated with a high quality management team, competitive advantage, good capital allocation etc.

They then use some more additional criteria to create a final list of 75-80 firms they can invest in. These additional criteria include robustness, high predictability (not a fast changing business), favourable business templates and finally the presence of costly signals. Let us quickly unpack these.

A robust business has made consistent operating profits over a long period, has a fragmented customer base (or no concentration in customer base), has no debt, excess cash, has moats (strong brand, industry with high entry barriers), has a fragmented supplier base, stable management team, and is in a slow changing industry.

They prefer slow stable businesses (electric fans over electric vehicles, he says) which don’t change fast (like Nokia).

Favourable business templates are those like job boards and yellow pages which see high profitability for the market leader (as opposed to airlines which are unprofitable mostly everywhere).

Costly signals are those which take time to reproduce like operating profits and hence honest signals versus signals such as PR announcements.

Thus, they have a final list of 75-80 companies they can invest in, and this constitutes their strike zone. They do not go outside these 75-80 companies ever. This is how they avoid big risks and identify high quality companies.

They wait for market crises (global financial crisis, COVID etc.) for price drops in these companies and they then buy large chunks of these companies. Almost half of their capital deployment of nearly $2b was done across three periods when the Indian stockmarket crashed (2008-09, 2011 and recently in 2020). 22% of the capital was deployed across three months of March to May 2020 he says, when high quality companies went on sale, and are available at fair prices. This waiting to strike is a feature of great investors. Bruce Karsh, cofounder of Oaktree Capital, alongside Howard Marks, similarly describes in How to Invest by David Rubenstein, how they invested large amounts to take advantage of favourable conditions for distressed debt investing in 2008-09 during the Global Financial Crisis, and in March-April 2020 as COVID derailed the financial markets.

They then seek to hold these companies forever (this is the lazy part). The final section of the book dwells into why they like to hold forever – because the best companies tend to persist, and compounding needs to be played out over a long period.

This is broadly how the book is structured. Each chapter has a principle or lesson from evolutionary biology, and tries to draw parallels to the investing world.

How Pulak’s principles compare and contrast with venture investing

It is interesting to contrast Pulak’s principle of eschewing Type I errors or errors of commission with venture, where errors of omission often matter more, because a large majority of the investment returns come from a few companies (‘The Power Law’). Errors of omission can be very costly here. Errors of commission are less costly in venture as one winner can cover losses from a multitude of bad bets. That said, I do wonder if the power law phenomenon applies to the Indian venture market entirely. My sense is that the Indian venture market exhibits a weak power law. The winners here aren’t necessarily as big as they are in the west.

My colleague Karthik Reddy, who cofounded Blume, likes to think of venture investing process as a two-stage process – the first where you ensure you avoid false negatives – that is, you ensure that there are no errors of omission, where you unwittingly pass on meeting a potential winner. The second stage is where you avoid a false positive or errors of commission, that is, picking the wrong company. A great venture investor tries to eschew both these risks and sets his or her investing process and style to eliminate these risks. I thought this framework was an interesting parallel to Pulak’s Type I and Type II errors framework.

A direct contrast of public market investing with venture investing can be misleading though. A big learning for me from my last few years in venture is that there is a two-tier market in venture, a lower-tier, less or non-venture-fluent founder market (almost always a first time founder, though some first-time founders are venture-fluent) and an upper-tier venture-fluent founder market (a lot of whom are second-time founders). In the lower tiers, the VC ‘picks’ the investment; it is effectively a buy-side business. In the upper tier venture market, the founder picks the VC or capital he wants to buy with his equity. It is sell-side effectively, and the VC is trying to make his or her brand of capital acceptable and attractive to the founder.

Interestingly, Alex Bangash of Transpose, a fund of funds platform, calls VC (essentially the upper tier venture market) an access class business, not an asset class business, given it is fundamentally around getting access to top-tier founders. He also refers to VC as the only asset class where the asset picks the manager and not the other way around. Thus, in my opinion, if we recognise the two-tier structure of venture as well as the access class theory, then a lot of the frameworks that inform public-market investing, and thereby Pulak’s frameworks thus cannot be directly employed in the upper-tier venture business, or at least there is no easy contrast.

For instance, take Nalanda’s reluctance to invest in fast-changing businesses. Venture is the opposite of this, in the sense that we like to skate to where the puck is, and our investors demand us to invest in fast-changing businesses. This principle along with how they prioritise risk of commission over omission, was I thought the biggest difference of Pulak’s principles with venture investing.

But there are also similarities in some areas. For instance, Nalanda’s reluctance to sell, which I found very impressive. In venture too, we are very reluctant to sell – lack of liquidity is one factor, but there is also the fact that given our business has a power law (even if weaker than in the west), the vast majority of returns comes from a few investments, and you don’t want to sell those too early.

One point I found amusing was that Nalanda’s returns despite being focused on high quality stocks, exhibited some signs of a power law (of course far weaker than in venture). Pages 254-55 of the book cover how some of their holdings have performed, and I thought it was interesting how a few of their investments account for disproportionate returns. While it isn’t a true power law like in venture, there are some resemblances. Page Apparels is their big winner; it has risen 82x over the near 14 years of their holding, while Berger for instance has only risen 32x in a similar time frame. Most of the other winners are in the 10-15x over 10-12 yrs range. There are seven stocks that have underperformed.

Finally, I thought it would be interesting to look at two areas that Pulak stresses to filter for high quality companies and see what the equivalents for venture are.

The first is ROCE in public companies. Wondering what it could be for venture investments. Could it be say being CM2 Positive on Capital Deployed (though this doesn’t factor in growth which is important)? Or is it NRR? Or perhaps it is not a business metric, but something like a second-time founder or some who is venture-fluent?

The second is signalling. What is honest and costly signalling? Clearly one could be opportunity cost foregone (like giving up a high-paying job); the others could be a very high ESOP pool to attract talent.

Am sure there are more examples here.

To sum up, Pulak’s book was extremely interesting and enlightening. To me what I took away is the importance of reducing errors of commission, limiting your strike zone to 75-80 companies, using ROCE and predictability (lack of change) as filtering mechanisms, concentrating buying in periods of market crises, and finally not selling ever.

Pulak is not well-known unlike say a Rakesh Jhunjhunwala or Shankar Sharma or a Porinju Veliyath. Hopefully this book will popularize his investment style, one of the most successful ones in the Indian public market investment space.

*

A summary of the book by me is here.

A Primer on PMF

Product-Market Fit (PMF) is my white whale and obsession. I am presently researching this topic for a (play)book I hope to publish for founders to systematically work towards hitting PMF. Meanwhile, I have compiled my research and explorations on PMF into a presentation for founders. Think of it as a primer on the topic, with a high-level overview of the steps involved and how to approach it, with some caveats. The presentation is proving to be popular. In the last couple of months, I have done three sessions where I showcase the presentation and clarify the concept for founders. You can see here for some key slides from the deck with my notes alongside, or view / download the full deck here.

PMF Convo #10 - Prukalpa Sankar, Atlan

I published a new PMF Convo, my #10th. This time it was with Prukalpa Sankar, the cofounder of Atlan (think of it very simplistically as Github for data teams, i.e., a collaboration hub creating context and trust for all members of the data science team). PMF Convos are 1:1 zoom or in person conversations I have with founders, operators, VCs as part of my research on PMF (product market fit). I transcribe these, and if the guest is willing, I release the edited transcript.

In our zoom conversation that we did mid-May, Prukalpa talks about the transition from SocialCops, a profitable fast-growing services play with finite limits on scale, to Atlan, a product co with theoretically no limits on scale. Prukalpa and Varun, her cofounder, were obsessed with scale and in that pursuit of that obsession, they had to take very tough calls, including deprecating two profitable but ultimately smaller scale ventures than Atlan. In honing in on Atlan, the founders spoke to over 150 data scientists to understand their workflows, and suss out their pain points. This deep understanding of user pain informed the product deeply, and clearly was a factor in its eventual success.

Over the course of the talk, Prukalpa covers her definition of PMF (pull, repeatability of motion), why founders selling is a dangerous crutch for the business especially when founders rely on selling largely to those they know, and her recommended resources for founders seeking PMF. I really enjoyed this candid conversation with Prukalpa, and came away deeply impressed with how in their pursuit of scale, they were willing to make hard sacrifices including shutting down profitable units, to focus on the one thing that could scale. I hope you do too.

Here is the link to the transcript of our convo, also shared on Linkedin as an article.

“Newsletter being written on a Bloomberg terminal in the style of a Roy Lichteinstein painting”; DALL-E.

Readings

Now to Part II of the newsletter where I share what I read and found interesting. Many of you know that I have been deliberately eschewing articles in favour of podcast transcripts (given the higher signal to noise ratio in these). That trend continues.

Here are five podcasts whose transcripts I enjoyed reading, with my learning notes on them. For the last two, I organised the transcript, as the podcast publisher doesn’t provide the transcript. You are welcome!

1/ Pete Kazanjy, Atrium, and author of Founding Sales, on the Lenny Rachitsky podcast

Relevant episode for founders of early stage SaaS / B2B companies as well as sales managers or leaders. Pete Kazanjy is well-known for his book Founding Sales which recommends that in early-stage companies, the founder(s) should take a lead in selling because at this stage, what you are looking for is insights and feedbacks that help you further refine the product and iterate to PMF, and the fastest feedback loop is when the founder is in front of the customer.

In the episode, Pete Kazanjy expands on the topic, and details how founders should set up and run the sales org (start with 2 junior folks who support you and then after 20-25 accounts are in and there is some consistency of closure, get a mid-level manager with experience), and importantly evaluate performance of the sales hires (See how consistently the customers are moving through the funnel. Is s/he not getting a second meeting? Or s/he is getting a lot of demos but faltering on the win rate there? In addition he explains why remote working is bad for young sales folks (weaker delayed feedback loops), what the scales for sales is (rapid rapport building) and finally his fave books (I didnt expect one of them to be The Goal).

The scales for sales is rapid rapport building. Scales as in Tyler Cowen’s questions to his guests “What is it you do to train that is comparable to a pianist practicing scales?”

Link to additional highlights.

2/ Fidji Simo, Instacart on Colossus’ Invest Like The Best w Patrick O’Shaughnessy

Enjoyed this a fair bit. Fidji is a super-operator who ran the Facebook app and now is CEO at Instacart. Very curious hire coming from a digital to a largely physical business, but certainly Instacart having a large and fast-growing ad busines helped (30% of overall revenues and growing per a recent report).

The podcast is interesting in that it gives you a sense of how Fidji and Instacart are thinking about driving the presently utilitarian product usage into higher value add experiences leveraging AI, data and consumer insight, such as “I want a birthday party menu for 15 kids and 5 adults” and for Instacart to suggest that and enable one-click ordering. There are many such ideas and experiences highlighting innovative product thinking scattered throughout the podcast such as the Instacart Health product where they will enable doctors to prescribe a diet like they prescribe medicine, and enable that to be provided via Instacart. It is also a useful lens to understand how an innovative player in the ecommerce space is thinking about leveraging AI.

Using AI at Instacart

Link to additional highlights.

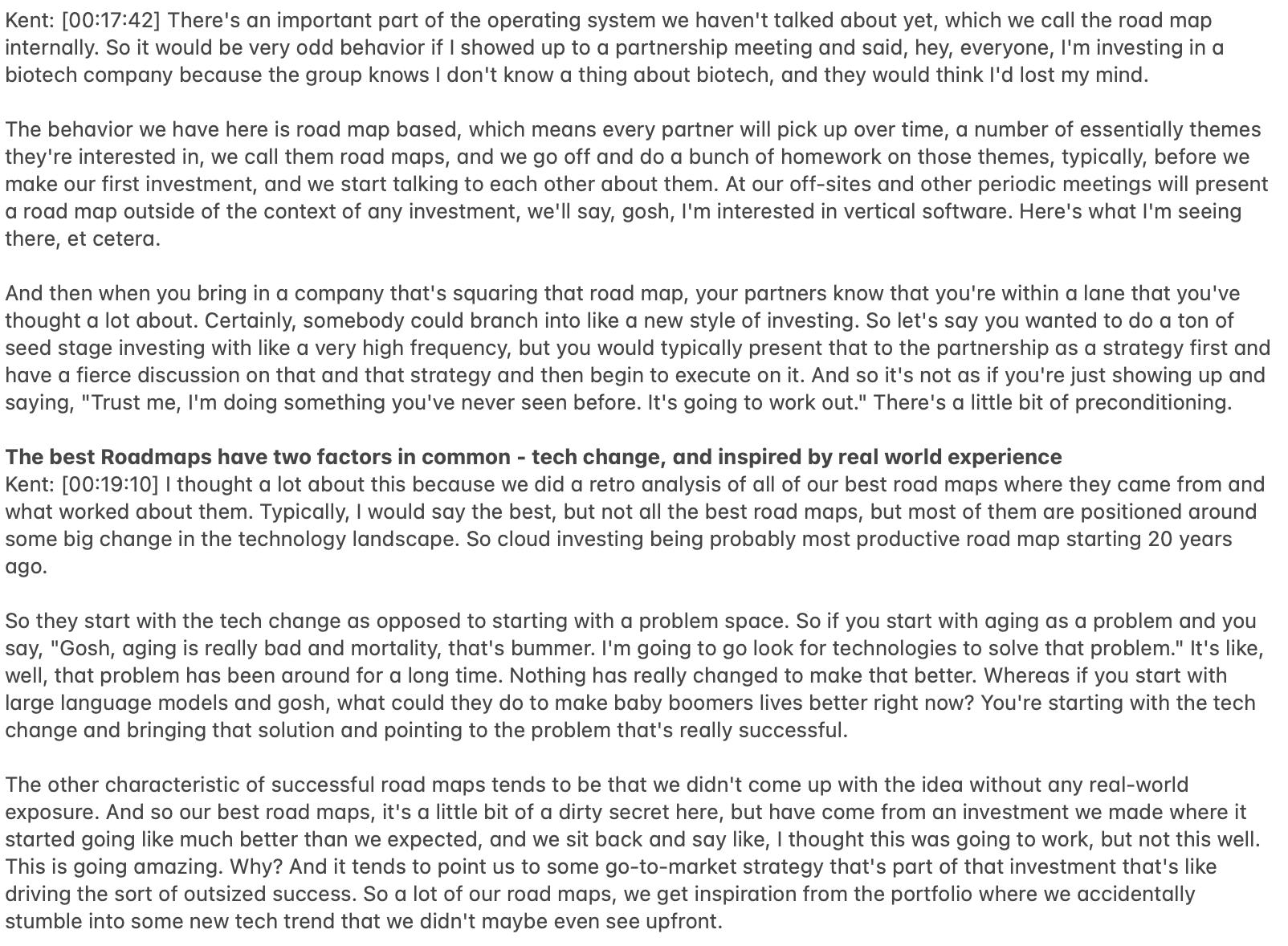

3/ Jeremy Levine, Kent Bennett, Brian Feinstein of Bessemer Venture Partners on Colossus’ Invest Like The Best w Patrick O’Shaughnessy

Bessemer Venture Partners is one of the OGs of the venture industry. Lots here to learn for a venture nerd like me, from this podcast where Patrick O’Shaughnessy hosts three of the senior partners at Bessemer including the legendary Jeremy Levine. I got to learn a lot about how they work together and the Bessemer OS. What I found particularly interesting - their investment decision-making structure, including the voting, the concept of roadmaps as a way to develop individual investor expertise in a sector (similar to Accel’s prepared mind), why they have a psychologist in each of their key meetings, how they groom and mentor the youngs, and how they look at content. Recommended for venture enthusiasts and VC partners.

Investment decisions and voting at Bessemer

Roadmaps or thesis-building at Bessemer

A psychologist attends key meetings at Bessemer!

Link to additional highlights.

4/ Anand Lunia, India Quotient on Speakeasy with Dheeraj Sinha

Enjoyed this conversation between Anand Lunia of India Quotient, one of the more original (and provocative) thinkers in the Indian startup ecosystem, and Dheeraj Sinha of ad agency Leo Burnett. This is not a new convo, it is over one and a half years old. I got this transcribed recently because I was meeting Anand as part of a group interaction, and I wanted to know his personality and investing style

a little better. It is excellent in that light, and doesn’t feel dated at all. Key takeaways include -

The rise of the ‘unempowered majority’ masses who are a new market for startups to chase

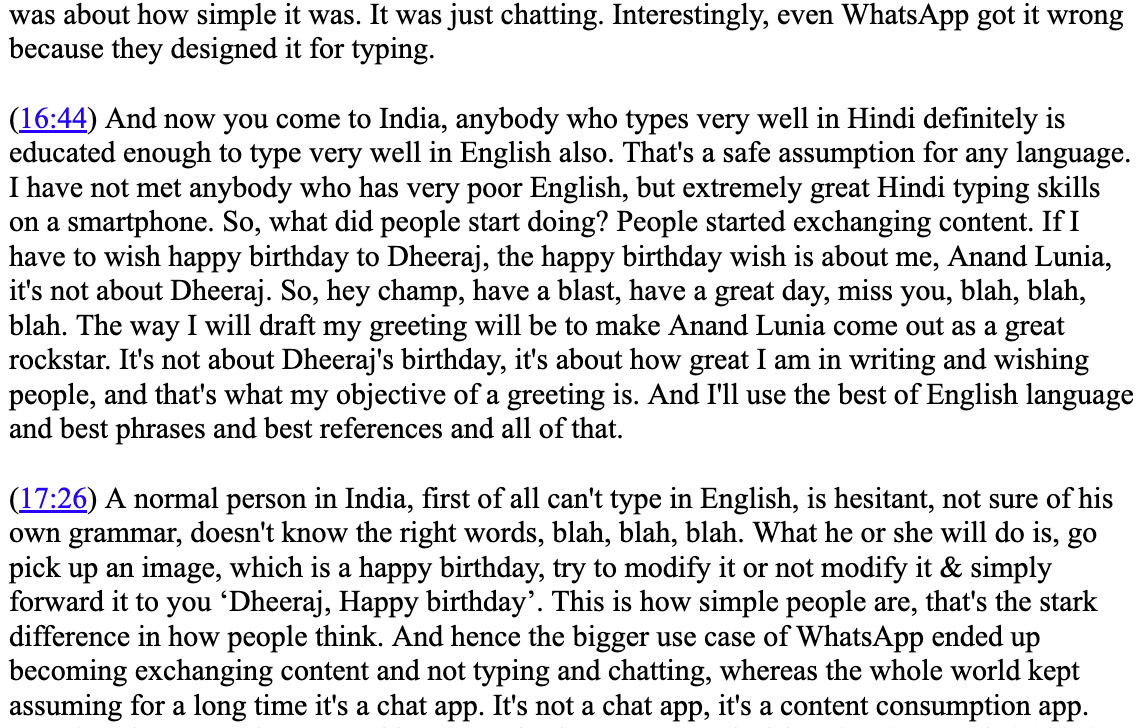

Lunia’s insight into how India2 / Bharat users feel comfortable sharing content more than typing (“…anybody who types very well in Hindi definitely is educated enough to type very well in English also. That's a safe assumption for any language. I have not met anybody who has very poor English, but extremely great Hindi typing skills on a smartphone. So, what did people start doing? People started exchanging content”)

how our default assumptions about UI / UX (email for log in, closing a browser window, browser and search bar) are all intimidating or strange for the new mobile user (the examples Lunia shares are fascinating)

why he thinks the next wave of D2C brands will be aimed at the affordable end of the market, why he is bearish on Thrasio (which turned out to be right)

and finally,

why he invests in founders who don’t need any help.

Whatsapp for content sharing, not typing.

Link to podcast | Link to transcript (organised by me as the publisher doesn’t provide a transcript).

5/ Sameer Brij Verma, Nexus Venture Partners on 1947 Rise with Shiva Singh Sangwan

Much like Anand Lunia’s podcast above, I organised the transcript of Sameer Brij Verma’s podcast given I was meeting him as part of a larger group, and wanted to know the man better. Sameer was riveting in that closed group setting, disarming us with his candour and impressing us with his insight and wisdom. He is much more guarded here, naturally, and the questions don’t probe too deeply, but the podcast is still useful to learn about his backstory, his entry into venture, the Nexus story. We also get a glimpse into the man himself, what he thinks is the best and worst about venture, and finally Sameer beyond venture. Enjoy.

Link to podcast | Link to transcript (organised by me as the publisher doesn’t provide a transcript).

Bye

In comparison to the previous newsletter, this was short! Ok, maybe not as much! As I shared earlier, you should think of this substack as akin to a monthly magazine - you don’t have to read it all in one sitting, and you don’t have to read all of it!

That is all for now folks. Feedback in the comments or at sp@sajithpai.com (Please don’t send pitches or CVs or anything work-related at my personal id; I may / may not respond to them; instead please use sp@blume.vc for pitches please).